Where did Disney and Live Nation’s missing $10 billion go?

In both economic and pandemic terms, we are in a relatively quiet period compared to the first half of the year. COVID-19 is at much lower levels in most countries and there are multiple sectors, such as housing and auto, that are reporting booms. These positive indicators will likely be both a pre-recession bounce and the lull before COVID-19’s second peak. However, there is a crucial subtext here, which is that one sector’s loss is often another’s gain. COVID-19 saw winners and losers, as any post-recession recovery is defined by ‘scarring’ where some companies and formats build where others have failed. For entertainment companies that lost revenue during the first half of the year, the question is whether they will regain that revenue or whether their lockdown legacy will be a long-term contraction.

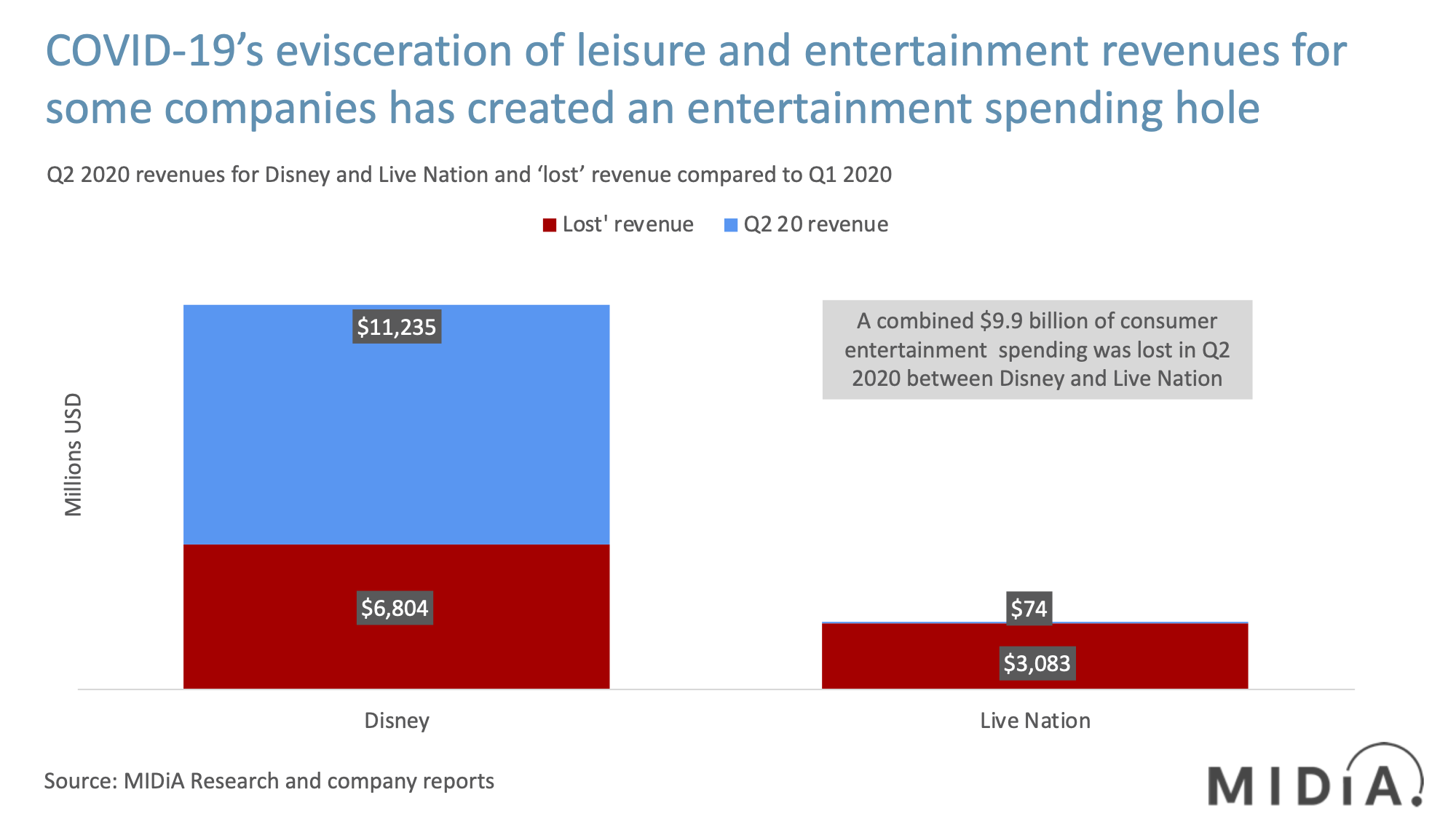

Live Nation and Disney (because of its theme parks) were two of COVID-19’s biggest and highest-profile entertainment company casualties. Live Nation’s revenues fell from $3.2 billion in Q2 2019 to $74 million in Q2 2020, a 98% decline. Disney’s fall was less in relative terms (-38%) due to having a diversified business but more than double Live Nation’s loss in actual terms. Between them, Disney and Live Nation lost nearly $10 billion of revenue which can be bluntly equated with $10 billion of consumer entertainment spend that went unspent in Q2 2020. The big question is whether that spend remains dormant, waiting to be tapped when doors open again, or has it gone elsewhere – and if so, can it be won back.

The lockdown winners were companies that could trade on consumers being cooped at home: games, video, home shopping, video messaging etc. Some of these were stop-gaps that consumers turned to in order to fill the void; others represent long-term behaviour shifts. Here are some of the places consumers shifted their spend, and how it might impact recovery for entertainment businesses:

Featured Report

Ad-supported music market shares Spotify ascending

Ad-supported streaming has always occupied a unique and slightly contentious place in the music industry ecosystem. On the one hand, ad-supported still represents an effective way to reach consumers at scale, creating a wider subscriber acquisition funnel.

Find out more…- Home improvements: One of the areas to see strong lockdown growth was home improvements – people stuck at home staring at the DIY jobs they had always meant to get around to doing and now had both the time and the money to do them. Home Depot saw its Q2 2020 revenues increase by $7.2 billion, nearly three quarters of that lost Disney and Live Nation revenue. Obviously, these are not like-for-like shifts as different geographies are involved, but the direction of travel is clear. The beauty of the home improvements business model is that there is always another room to do, another project to start. The risk for entertainment companies is that a portion of these new home improvers may have got the DIY bug and will have less spend to shift back to entertainment.

- Home shopping: Amazon was a huge lockdown winner, growing quarterly revenues by 42% compared to 2019, representing an increase of $38.3 billion. Those revenues include, among other things, its cloud business, which rode the wave of many of lockdown’s other success stories. Additionally, the shift to home shopping has been pronounced. Amazon’s growth has extra implications for entertainment companies. Its subscriptions were up 29% which largely refer to Amazon Prime, which of course comes with music and video bundled in and will in turn compete directly with pure-play propositions like Spotify and Netflix. This will take on added significance during the recession: when cost-conscious consumers are forced to cut back on spending, an all-in-one entertainment bundle that includes home shipping looks a lot more cost effective than a handful of standalone subscriptions. Amazon Prime is not recession proof, but it is certainly recession resilient.

- Changing of the guard: Some of most interesting shifts are actually within entertainment. For example, AMC cinemas saw quarterly revenues fall by a catastrophic 99%, representing a quarterly loss of $1.5 billion while over the same period Netflix gained $1.3 billion. Again, the geographies are not directly comparable but the direction of travel is clear: old video being replaced by new video. A similar changing of the guard is happening in digital advertising. Alphabet, the powerhouse, saw revenues fall by 2% while Amazon saw its ad revenues grow by 40%. Turns out that advertisers will pay a premium to reach customers that are one click away from a purchase. Who’d have thought it…

The list of examples of lockdown shifts goes on and on. In fact, so much so that MIDiA is currently working on a major new piece of research exploring these shifts and what the long-term implications are for entertainment businesses. We’re calling it ‘Post-Pandemic Programming’. There will be a series of in-depth reports for clients and also a webinar and podcast mini-series. So, watch this space!

But returning to the above findings, the key takeaway is that companies that lost entertainment spend during lockdown should not assume that this spending is waiting in consumer’s bank accounts, ready to be spent as soon doors open again. Pent-up demand will ensure much of it will but some of it is probably gone for good, allocated to new habits developed during lockdown but that will persist long after. This is not to say that those companies cannot return to previous heights, but to do so they will need to unlock new spending from new customers. Which may not be the easiest of tasks during a global recession.

Want the latest entertainment research and insights directly to your inbox? Our newsletter has you covered, click here to subscribe.

The discussion around this post has not yet got started, be the first to add an opinion.