We pinpointed the right price for Super Premium. Here is how

Photo: MIDiA Research

There is broad consensus across the music industry that it is time to introduce new tiers for streaming, including one with extra benefits that is often nicknamed “Super Premium”, or “Supremium” for short. But putting this into practice gets complicated pretty quickly.

It would be great if we could simply survey consumers about their interest in Supremium at a certain price. Unfortunately, this type of surveying is highly susceptible to over-reporting and lacks the nuance needed to unlock actionable insights (especially with so much riding on the potential success of Supremium).

Complex problems require complex solutions. This is why MIDiA embarked on a landmark streaming pricing study of 2,000 US consumers, fielded in Q3 2024. The results allow us to understand not only subscribers’ willingness to pay for a Supremium tier at a granular level, but also to pinpoint the exact price that would maximise revenue for streaming services.

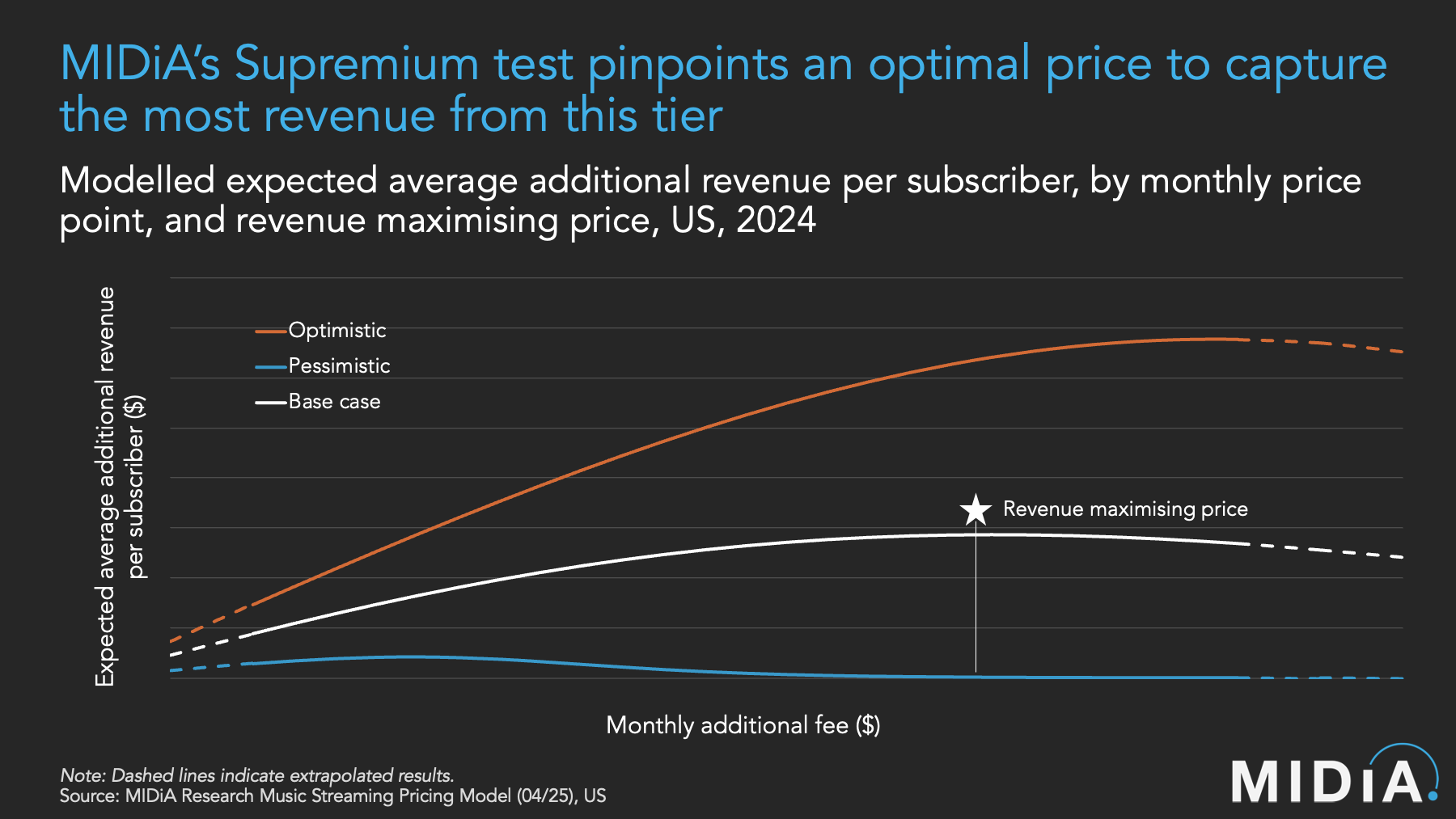

And revenue maximisation is the cornerstone of this work. Finding the maximum some people will pay is not the same thing as finding the – possibly lower – price point which will generate more total revenue, because the extra number of people paying will offset the slightly lower average revenue per user (ARPU).

Not only did we test Supremium – we also tested willingness to pay for a standard subscription; an “ad-lite” tier; and to pay the whole year of premium upfront.

The full report, 'Breaking saturation | Music streaming pricing strategy', is out today. Here is how we did it, and a sneak peek at what we found.

Featured Report

Music subscriber market shares Q4 2024 Full stream ahead

Streaming market metrics are bifurcating. Label streaming revenues were up in 2024, indicating a much anticipated slow down in revenue growth. Yet, at the same time, music subscriber growth was nearly...

Find out more…How the study works

MIDiA’s pricing study is a variant on the Gabor Granger methodology:

- First, subscribers were asked to their overall level of interest in a Supremium tier unlocking extra benefits like early access to music and hi-fi audio, on a five-point scale

- Next, subscribers with non-zero interest were asked if they would pay for Supremium at a certain price – say, $5.99

- If the respondent answered yes, they were next asked if they would pay for it at a slightly higher price – say, $6.99

- If the respondent answered no, they were next asked if they would pay for it at a slightly lower price – say, $4.99

- This process was repeated until the maximum price the respondent would pay was determined

- Next, our model allocated a value for willingness to pay to each respondent, at each price. This accomplishes two things: It places a realistic downweight on the responses given (recognising that consumer surveys tend to over-report); and factors in each respondent’s level of interest in the proposition (e.g., “very interested” is more likely to translate to purchasing behaviour than “somewhat interested”).

Then, we calibrated these inputs against other MIDIA sources, including against our music subscriber market shares data. For example, the number of non-subscribers willing to pay $11.99 in our test broadly aligns with total US subscriber growth over the past year.

Willingness to pay values for each respondent were then collated and used to train a logistic regression model, which allows interpolation and extrapolation to a range of different price points. At last, this unlocked a revenue maximising price for each proposition. Alongside our “base case” model, we also created optimistic and pessimistic cases. Only after all of these steps could we feel confident in our results.

What did the study reveal?

With such valuable insights, there is little we can share publicly. But here is a sneak peek. The Supremium study reflects promise: just under-three quarters of music subscribers have some level of interest in paying for Supremium as an add-on. Base case willingness varied from just over one-fifth at a $1.99 additional fee, to 10% who would be willing to pay more than double the cost of their monthly subscription.

But the study gets even more interesting when we explore the trade-offs between revenue growth and subscriber growth. Should services cut their prices to get subscribers on board, and by how much? Is it worth taking a hit on discounted annual plans to offset churn? The report reveals the impact of a range of pricing decisions on revenue and subscribers.

Our study also flags future challenges, such as the paradox streaming services face with Supremium: offering perks like early access to merchandise and tickets at scale, while retaining perceived value. If the product really takes off, early access for everyone effectively becomes early access for no one. In this way our study answers critical questions, as well as asks new ones. Our homework on pricing is done, but the larger test is just beginning.

'Breaking saturation | Music streaming pricing strategy' is available for MIDiA clients here. For more information on how you can access this report, please reach out to enquiries@midiaresearch.com.

The discussion around this post has not yet got started, be the first to add an opinion.