The Spotify Numbers You Won’t Have Seen

One of the core values that we deliver to our clients at MIDiA Research is finding the ‘third number’— the data point that wasn’t reported by a company but that can be arrived at through a process of modelling and triangulation. Next week, we will publish a report that does just this for the numbers presented in Spotify’s F1 filing. The metrics we arrive at help create a more complete picture of Spotify’s performance for investors and rights holders, as well as the impact of core metrics upon other parts of Spotify’s business. In advance of its publication, here are just a few highlights.

Spotify’s F1 filing paints a picture of a growing business that is improving metrics across the board, with the foundations for a solid couple of years ahead now well built. But there are also a number of challenges:

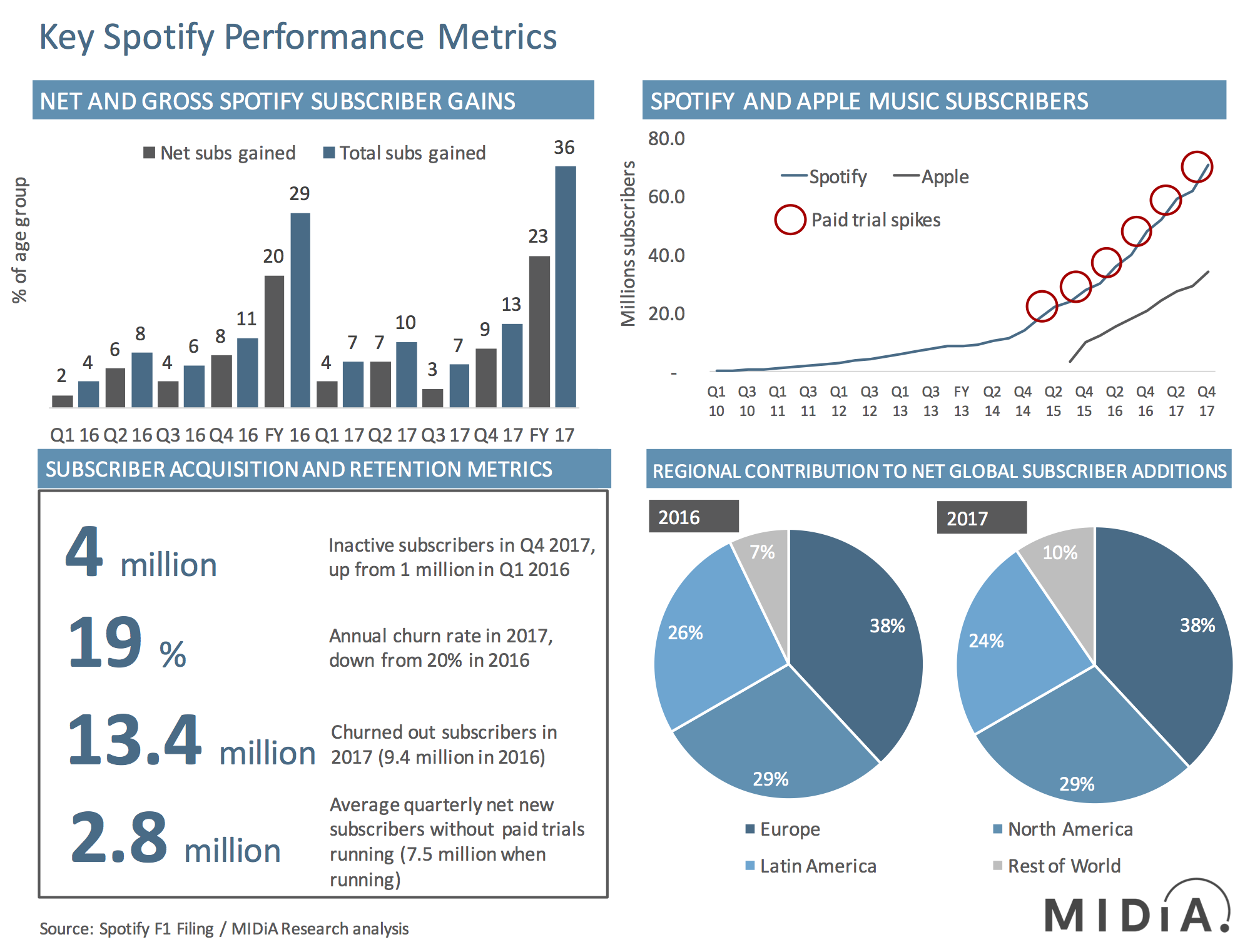

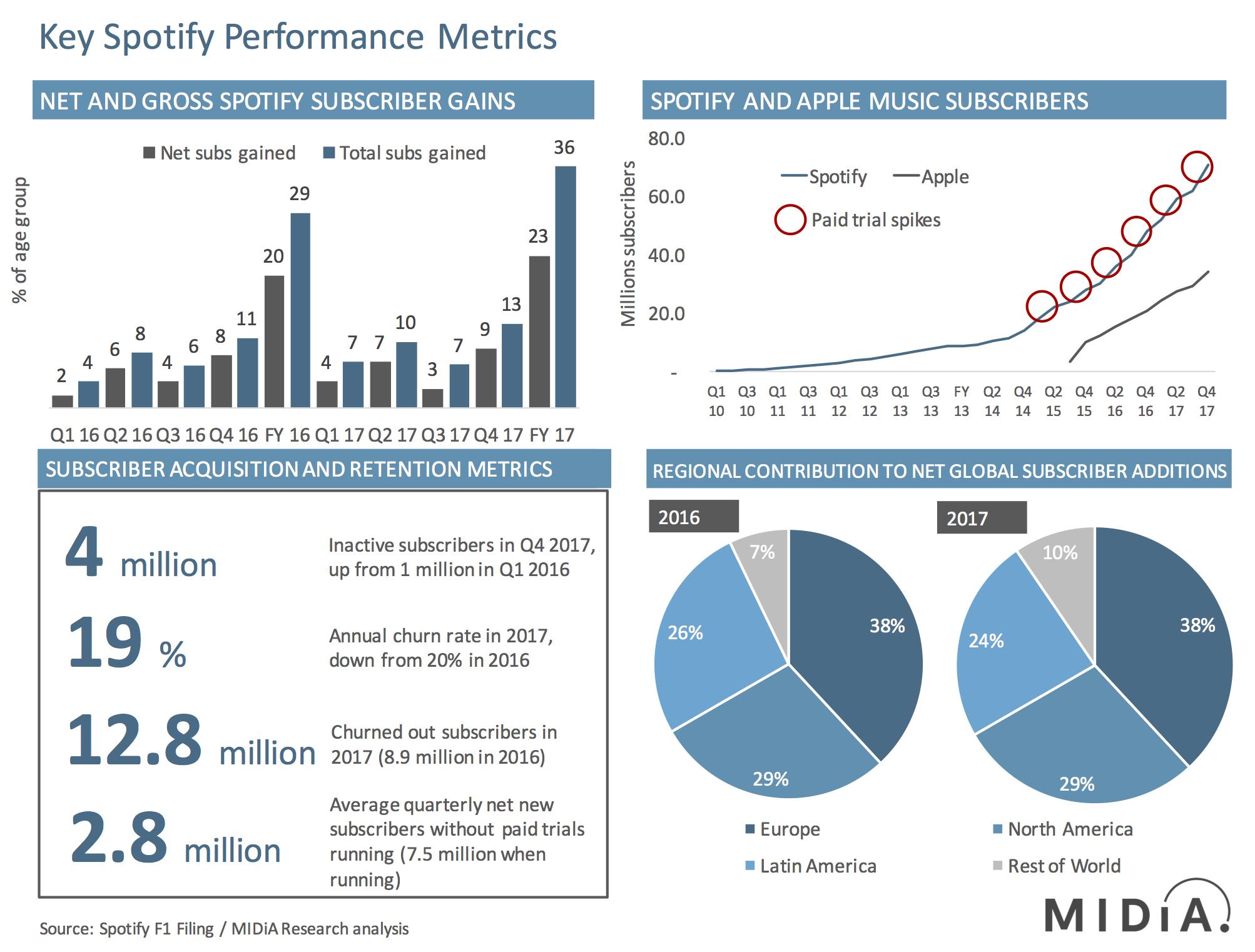

- User growth: Spotify experienced strong growth between Q4 2015 and Q4 2017, increasing its subscriber base from 28 million to 71 million, its ad supported users from 64 million to 92 million and its total monthly active users (MAUs) from 91 million to 159 million. Set in the longer-term context, Spotify’s subscriber growth trajectory indicates it is well up the growth curve, with 2014 representing the earlier growth phase and Q1 2015 the point at which the inflection point occurred. Since Apple Music entered the market in mid 2015, Spotify has seen growth actually increase, and over the period added more net new subscribers by the end of 2017 (49 million) than Apple Music did (34 million).

- Streams up, but inactive subscribers also: Engagement is growing, with subscribers playing an average of 630 streams a month in 2017 compared to 438 in 2015. Over the same period ad supported users increased average monthly streams from 119 to 222. The net result was 195.4 billion streams in 2017 compared to 59.6 billion in 2015. However, inactive subscribers (i.e. subscribers plus ad supported users minus MAU) grew from one million in Q1 2016 to four million in Q4 2017. Though this is a long way off the ‘zombie users’ problem that Deezer has historically suffered from due to inactive telco bundles, it is a metric Spotify will need to keep on top of.

- Churn down…: Throughout 2016 and 2017 Spotify progressively reduced its churn rate from 6.9% for Q1 2016 to 5.7% in Q4 2017. This is despite churn being pushed up by the super trials and thus reflects a solid improvement of organic retention across Spotify’s paid user base. In a March investor presentation, CFO Barry McCarthy argued that as Spotify’s subscriber base matures, life time value (LTV) and gross profit will increase, with more subscribers sticking around for longer.

- …but not out: Despite quarterly falls, churn remains a core issue while Spotify is in growth phase and is acquiring portions of subscribers who try out the service but realise it is not for them. On an annual basis churn 18% in 2017, down from 18.5% in 2016. These lost subscribers totalled 12.8 million in 2017, up from 8.9 million one year earlier. Spotify added 23 million subscribers to its year-end total in 2017 but, including churned out subscriber the total subscribers gained was 35.8 million. Thus, churned subscribers accounted for 36% of all subscribers gained. This process of getting more subscribers in than out is common to all premium subscription businesses and is particularly pronounced when a service is in growth phase, as is the case with Spotify. It is even more pronounced in contract-free subscriptions. Pay-TV and mobile companies have the benefit of long-term contracts to minimise churn. The fact that Spotify reports churn at all is creditable. McCarthy’s old company Netflix got so fed up with investors’ reactions to churn that it stopped reporting it all together.

- Super trials: Spotify’s subscriber growth has not however been linear. Heavily discounted trials offering three-month subscriptions for $1 have been pivotal in driving strong user growth spikes each quarter in which they run. On average, Spotify’s global subscriber base grew by a net total of 2.8 million each quarter between Q4 2015 and Q4 2017 in the quarters that these ‘super trials’ were not running, but by 7.5 million in the quarters that they did.

- Non-linear growth affects all regions: In 2016 and 2017, Spotify’s European and North American subscriber bases each grew at an average of one million subscribers in quarters without trials and three million and two million respectively in quarters with them. Thus, Spotify’s organic net monthly subscriber growth in each of these regions was around 330,000. A similar trend appeared in Latin America – where net subscriber growth doubled in each trial quarter from one to two million. The impact is more dramatic in rest of world, where rounded net subscriber growth was flat in all quarters without trials and more than one million in quarters with.

Despite the joint effects of subscriber bill shock and reduced margins, super trials are clearly net positive for Spotify’s business. When it later decides to fade them out in more mature markets – namely when it switches from user acquisition to user retention mode – Spotify will be able to quickly improve both margin and retention.

Barring calamity, Spotify looks set to have a strong 2018 in terms of growth across subscriptions, MAUs and revenue. If it continues its current operating strategy Spotify should reach 93 million subscribers by the end of 2018. By comparison, Apple Music is likely to have hit around 56 million subscribers by Q4 2018, with its rate of net new monthly subscribers having increased to 2 million in 2018.

If you are not yet a MIDiA subscription client and would like to find out how to get a copy of the forthcoming seven-slide report and accompanying dataset, email stephen@midiaresearch.com

The discussion around this post has not yet got started, be the first to add an opinion.