Recorded music market 2022 | Reality bites

Following a spectacular year of growth in 2021, global recorded music revenue growth slowed significantly in 2022 due to the combined impact of global economic headwinds and growth slowdown in mature streaming markets. Context, though, is everything – not many industries can deliver solid growth while the global economy is in turmoil, ad markets are falling and many emerging tech sectors are in crisis.

Global recorded music growth has oscillated in recent years, slowing in the pandemic, booming in 2021, and then returning to more modest growth in 2022.

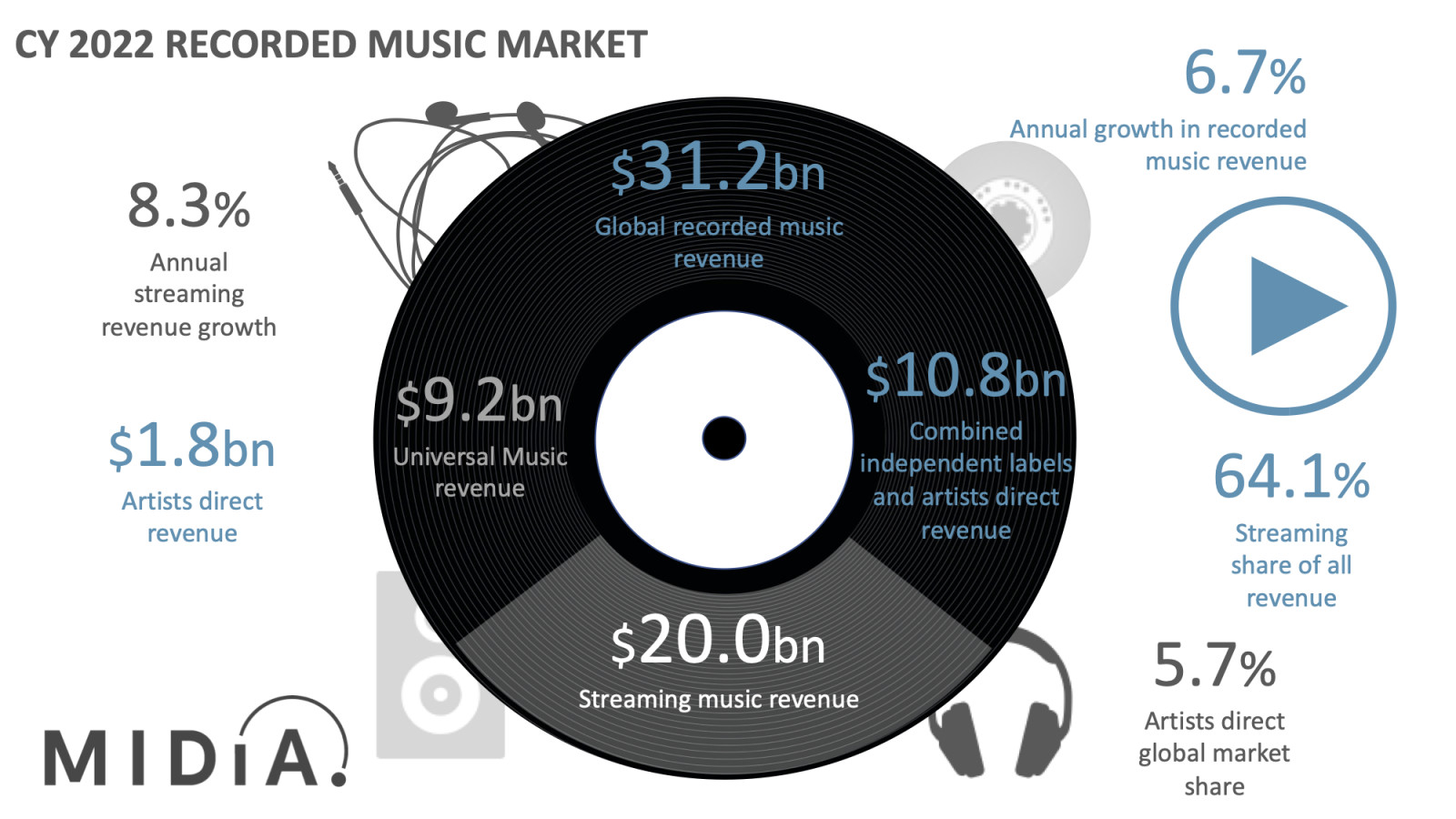

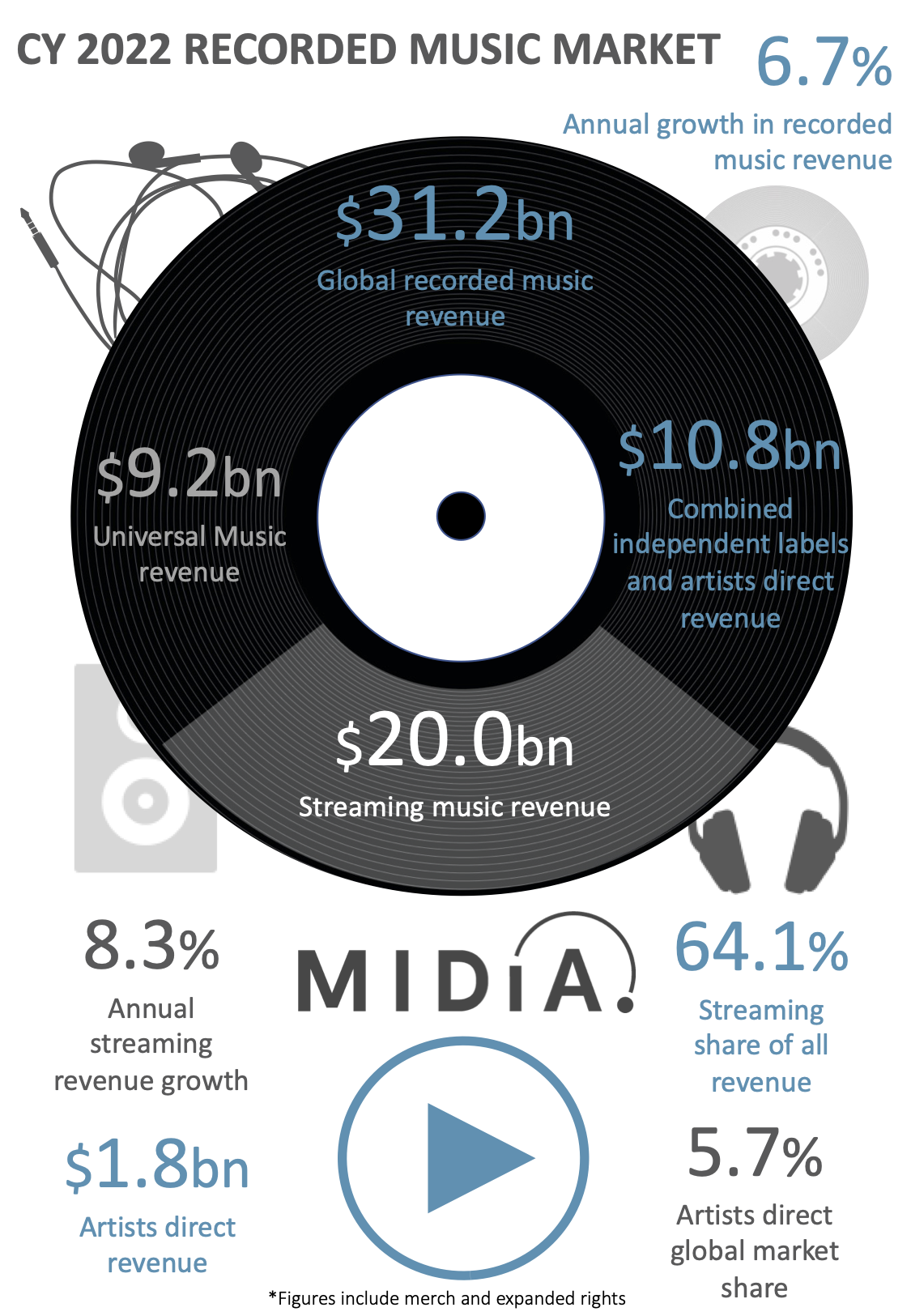

2022 was a year of realignment for much of the global economy, and the music business had to contend not only with the wider trend of the cost-of-living-crisis, but also rising interest rates softening music catalogue M+A demand and the long expected streaming slowdown kicking in. It is testament to the solidity of the recorded music market that, despite these multiple headwinds, global revenues grew by 6.7% to reach $31.2 billion in 2022. While this was significantly down on the 24.8% registered in 2021, it illustrates the strong role music plays in consumers’ lives, especially in uncertain times when escapism and identity are more important than ever. The persistent value of music was even more strongly illustrated by music publishing, which grew by 16.6% in 2022.

Streaming was again the main driver of industry growth, with revenues up by $1.5 billion in 2022 (8.3% growth), though this was less than half the $4.2 billion added in 2021. The slowdown was underpinned by a) slowing subscriptions growth in mature markets; b) a slowdown in ad-supported revenues, reflecting wider advertising market dynamics. Music subscriber growth was markedly stronger, up by 13.7% to 652 million, however, the more mature North America and Europe regions accounted for just a third of the growth. Emerging markets will become a progressively larger part of global streaming growth, but due to lower ARPU and low shares of Anglo repertoire, the divergence between growth revenue and subscriber growth rates seen in 2022 will become a long-term market characteristic.

Independent labels and artists direct both strongly out-performed the wider streaming market, growing streaming revenues by 13.9% and 17.9% respectively. In terms of total recorded music revenues,

Featured Report

Global South rising Streaming audiences in China, Turkey, and South Africa

It is increasingly clear that the future of the global music streaming business relies heavily on the Global South markets, which include Latin America, Asia Pacific, and the Rest of World. Most subscription...

Find out more…UMG added more recorded music revenue in 2022 than the other two majors, adding $0.5 billion to reach $9.2 billion, giving it a 29.5% share of the global recorded music market. UMG’s percentage growth (6.2%), though, was slower than SMG’s (8.7%), with SMG gaining 0.4 points of market share.

Artists direct (i.e., artists who release without labels, directly via a distributor) were the big success story once again, growing by 16.6% in 2022 to generate $1.7 billion of recorded music revenue, giving it a 5.7% market share, up from 5.2% in 2021.

Independent labels also outgrew the wider market (up by 7.1%), and the combined market share of artists direct and independent labels reached 34.6% in 2022, up from 34.0% in 2021. Though it is worth noting that this does not include the additional revenue from independent labels distributed by major labels.

Combined, independent labels and artists direct, were the largest single market segment with $10.8 billion.

Though overall market growth was down in 2022 compared to 2021, 2021 was in many respects a year of artificially accentuated, post-Covid growth, while 2022 was at the opposite end of the scale, with a host of economic headwinds. In this context, 6.7% growth for 2022 could be considered even more of an achievement than the 24.8% achieved in 2021.

The full report and dataset (with quarterly revenue by segment and format going back to Q1 2015) will be shortly available to MIDiA clients. If you are not a MIDiA client and would like to learn how to get access to our research, data and analysis, email stephen@midiaresearch.com

The discussion around this post has not yet got started, be the first to add an opinion.