PLAY – music’s next chapter

31 Jan 2024

Tags

The old maxim that change is the only constant feels tailor made for the 21st century music business. No sooner does the industry get its head around one paradigm shift then another one comes along. First piracy, then downloads, then streaming, then the rise of the independent artist and now…well, just what is ‘now’? AI may be the word on everyone’s lips, but as transformational as it will be, it is going to be an enabler of a wider shift, one that will see a forking from today’s LISTEN-focused ecosystem, resulting in the emergence of a new, parallel PLAY-focused one.

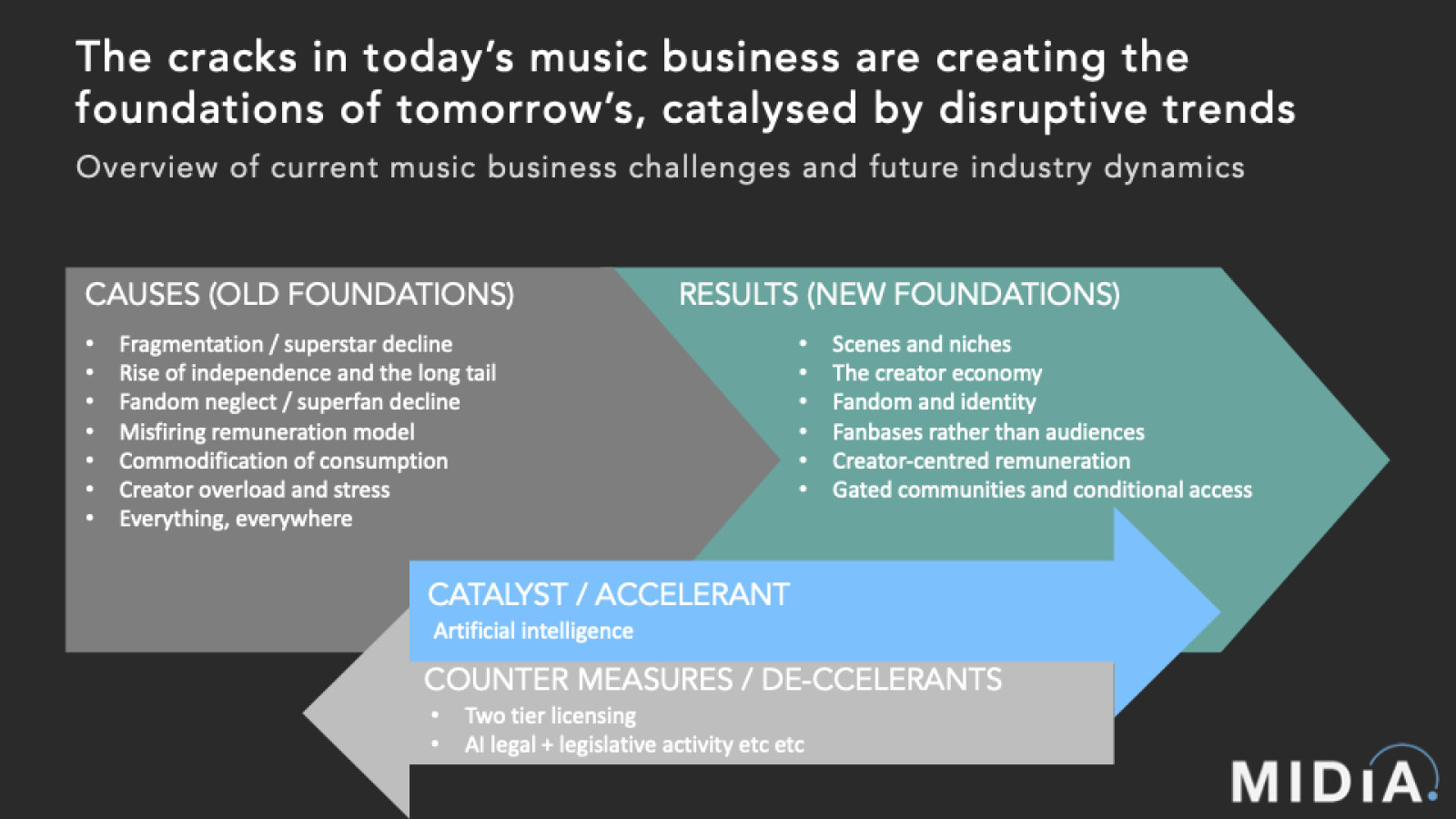

Streaming has achieved much and will achieve more. But it is becoming increasingly apparent that it is hitting limits, as illustrated by slowing growth in mature markets and the growing number of cracks in the system:

- Fragmentation of consumption and the decline of the superstar

- The continued rise of independent creators and growth of the long tail

- Fandom’s near-absence from streaming and the decline of the superfan

- A misfiring remuneration model with all stakeholders complaining about something

- The commodification of consumption

- Creators feeling unable to keep up with the demands of the ‘always-on artist’ model

- The everything, everywhere approach decimating scarcity and specialness

These fracture lines are not only not going to go away, they are simultaneously creating the conditions for what comes next. Many of these second-order consequences are already established, while others are yet to come to fruition:

- Scenes are flourishing as social algorithms push us ever closer to our niches

- The music creator economy is increasingly growing outside of streaming

- Fandom and identity are finding new places and voices

- Artists want fanbases they can connect with rather than anonymous audiences

- User centric and artist centric are still both rightsholder-centric models, creators want remuneration models that put then at the centre

- From private social groups to Discord servers, creators are realising the value of gated communities and conditional access to their music

Streaming has become more lean back at just the time that consumers, across the rest of their digital lives, have become more lean in. The good news is that this has enabled music to soundtrack to those lives, becoming the background activity. The less positive news, apart from the further commodification of consumption, is that because subscription royalty pots are finite, this means lower per-stream rates and putting even more distance between passive consumption and music fandom. As paradoxical as it may sound, the price of more listening can actually be less fandom.

Change, though, needs not only conditions but a change agent also. This is where AI steps in. AI itself will not create the next chapter of the music business, but it will help bridge the gap between today’s pain points and tomorrow’s growth dynamics.

Of course, talking about AI as a thing, is probably about as useful as talking about the internet twenty years ago. And just like then, even the most educated guesses about what it will become will fall far short. It is probably safest to think about AI as a foundational set of technologies that will form some of the backbone of tomorrow’s internet. And if we translate that pervasive impact to music, then we should expect it to shape composition, creation, marketing, distribution…basically everything, in some way, most often improving workflows rather than replacing them.

Featured Report

Ad-supported music market shares Spotify ascending

Ad-supported streaming has always occupied a unique and slightly contentious place in the music industry ecosystem. On the one hand, ad-supported still represents an effective way to reach consumers at scale, creating a wider subscriber acquisition funnel.

Find out more…The result of all this will be the forking of the music landscape into two lanes:

- LISTEN: today’s lean-back model that has become the long-term successor of radio (only much better monetised)

- PLAY: platforms that utilise AI tools to provide end-to-end, creation-to-consumption, bypassing the traditional DSP supply chain, and therefore, potentially sidestepping much of the rights world also. (TikTok’s negotiating clash with UMG may be a first step in this direction). The biggest difference that consumers will notice is that they can lean in and participate, both with artists’ content and by creating themselves.

The 19th century composer John Philip Sousa said of Eddison’s phonograph (the prime mover of today’s music business): “it is a horrible machine for bringing dead sounds back to life”. Consider that for a moment. Today’s recorded music and streaming businesses are built around dead sounds. Until recordings turned songs into creative full stops, music never ever sounded the same twice. PLAY services will help take music back to those pre-recorded days, making it something that is always evolving, often ephemeral and, crucially, something that everyone can take part in.

This might sound like a licensing quagmire, because it is. Music licensing hasn’t even yet figured out how to license the input phase of generative AI (i.e., the learning). It has certainly not started addressing what sort of rights framework should be put around the output (i.e., the music that people, including consumers, make with AI). The rights frameworks that will work for the PLAY era will need designing from scratch.

PLAY will become music’s cultural playground, the space where music will be an expressive, ever-changing medium and the traditional confines (genre, track length, structure, etc.) need not apply.

LISTEN will not go away, of course. Streaming will remain the bedrock of consumption. But alongside it, music will have a new lane. Streaming redefined the future of the music business, and although it also helped reshape music, it was never intended to. PLAY is different. The very essence of it is to reshape the future of both the business and culture of music. PLAY will redefine the future of music itself.

MIDiA clients: we’ll be exploring these ideas in much more detail and presenting a framework for how this will work, in a forthcoming report.

Want the latest entertainment research and insights directly to your inbox? Our newsletter has you covered, click here to subscribe.

The discussion around this post has not yet got started, be the first to add an opinion.