Music Subscriber Market Shares H1 2019

5 Dec 2019

Companies

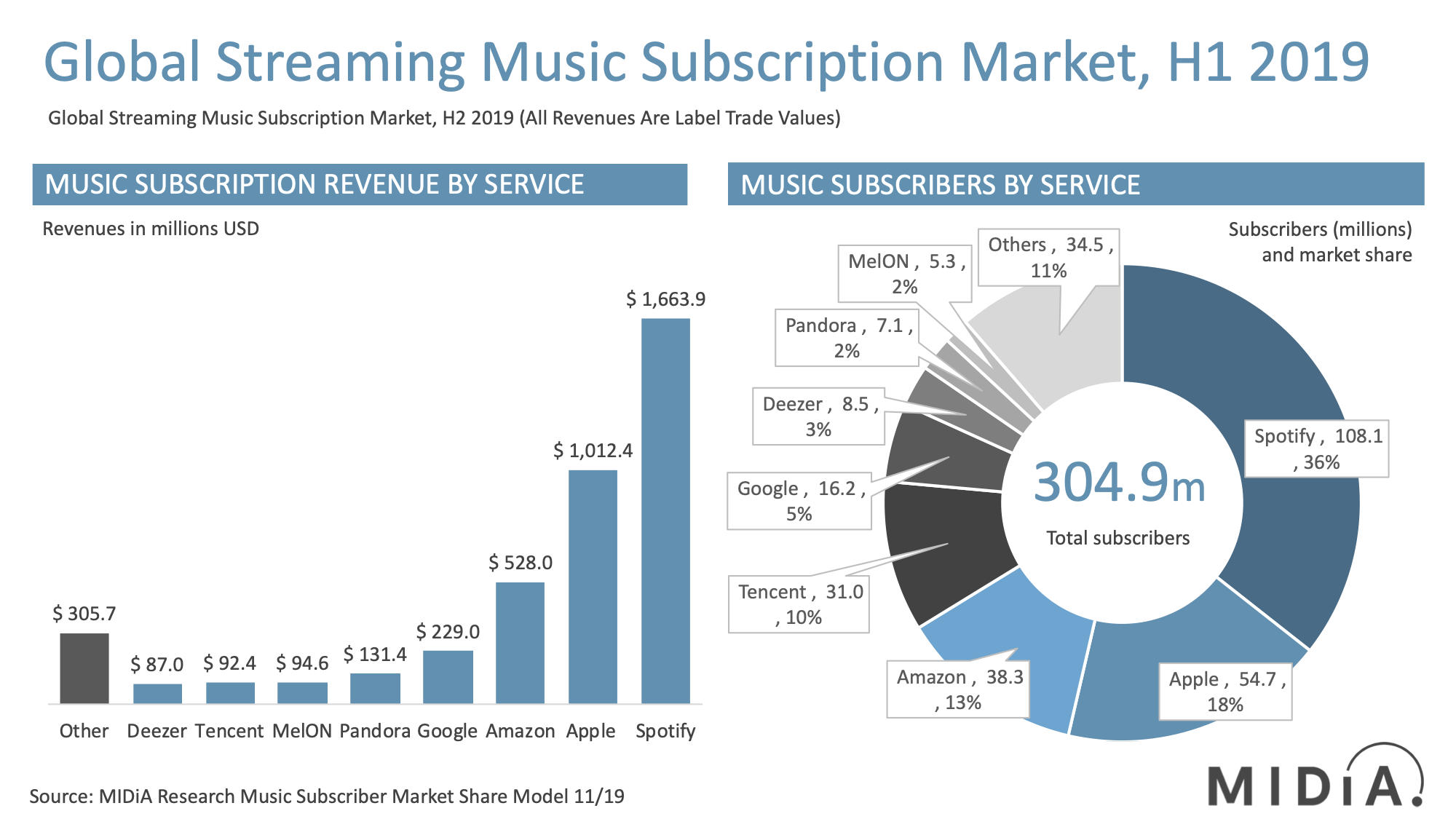

The global streaming market continues to grow at pace. At the end of June 2019 there were 304.9 million music subscribers globally. That was up 34 million on the end of 2018, while the June 2018 to June 2019 growth was 69 million – exactly the same rate of additions as one year earlier.

Spotify remained the clear market leader with 108 million subscribers, giving it a global market share of 35.6%, exactly the same share it had at the end of 2018 and at the end of 2017. In what is becoming an increasingly competitive market, Spotify has continued to grow at the same rate as the overall market.

Meanwhile both Apple and Amazon have grown market share, though Apple is showing signs of slowing. At the end of 2017 Amazon (across all of its subscription tiers) had 11.4% global market share, pushing that up to 12.6% by end June 2019 with 38.3 million subscribers. Apple went from 17.3% to 18% over the same period – hitting 54.7 million subscribers, but while Amazon added share every quarter, Apple peaked at 18.2% in Q1 2019 before dropping slightly back to 18% in Q2 2019. Though at the same time, Apple increased market share in its priority market – the US, going from 31% in Q4 2018 to 31.7% in Q2 2019 with 28.9 million subscribers.

Google has been another big gainer, particularly in recent quarters following the launch of YouTube Music, going from just 3% in Q4 2017 to 5.3% in Q2 2019. Google had a well-earned reputation for being an under-performer in the music subscriptions market, a company that did not appear to actually want to succeed. Now, however, Google appears to be far more committed to subscriptions, pushing both YouTube Premium and YouTube Music hard, with a total of 16.9 music subscriptions in Q2 2019, compared to just 5.9 million at the end of 2017.

Featured Report

Ad-supported music market shares Spotify ascending

Ad-supported streaming has always occupied a unique and slightly contentious place in the music industry ecosystem. On the one hand, ad-supported still represents an effective way to reach consumers at scale, creating a wider subscriber acquisition funnel.

Find out more…With the big four all gaining market share, the simple arithmetic is that smaller players have lost it. The share accounted for by all other services fell from 32.8% end-2017 to 28.4% mid-2019. This of course does not mean that all of these services lost subscribers; indeed, most grew, just not by as much as the bigger players. Of the other services, most are large single-market players such as Tencent (31 million – China), Pandora (7.1 million – US) MelOn (5.3 million – South Korea) with Deezer now the only other global player of scale (8.5 million).

In summary, 2019 was a year of growth and consolidation, with the global picture dominated by the big four players and Spotify retaining market share despite all three of its main competitors making up ground. 2020 is likely to be a similar year, though with a few key differences:

- Key western markets like the US and UK will likely slow from Q4 2019 through to 2020. Meanwhile, emerging markets will pick up pace

- This could shift market share to some regional players. For example, in Q3 Tencent’s subscriber growth accelerated at an unprecedented rate to hit 35.4 million subscribers. Tencent could be entering the hockey stick growth phase, and at just 2.6% paid penetration there is a LOT of potential growth ahead of it

- Bytedance could create a new emerging market dynamic with its forthcoming streaming service. Currently constrained to India and Indonesia, Western rights holders may remain cautious about licensing it into Western markets. The unintended consequence is that the staid western streaming market could by end 2020 be looking enviously upon a more diverse and innovative Asian streaming market

These figures and findings are taken from MIDiA’s forthcoming Music Subscriber Market Shares, which includes quarterly data from Q4 2015 to Q2 2019 for 23 streaming services across 30 different markets. The data will be available on MIDiA’s Fuse platform later this week and the report will follow shortly thereafter.

Want the latest entertainment research and insights directly to your inbox? Our newsletter has you covered, click here to subscribe.

The discussion around this post has not yet got started, be the first to add an opinion.